The Big Story

Quick Take:

-

Median home sale prices bounced back in a big way in April, as the spring selling season kicked into gear with nearly a 1% year-over-year increase.

-

Inventory levels continue to climb, with new listings pouring onto the market as sellers look to capitalize on the busier spring months.

-

Existing home sales are essentially flat on a year-over-year basis, as rising mortgage rates give buyers a reason to pause.

Note: You can find the charts & graphs for the Big Story at the end of the following section.

*National Association of REALTORS® data is released two months behind, so we estimate the most recent month's data when possible and appropriate.

Spring has sprung, and so have median sale prices

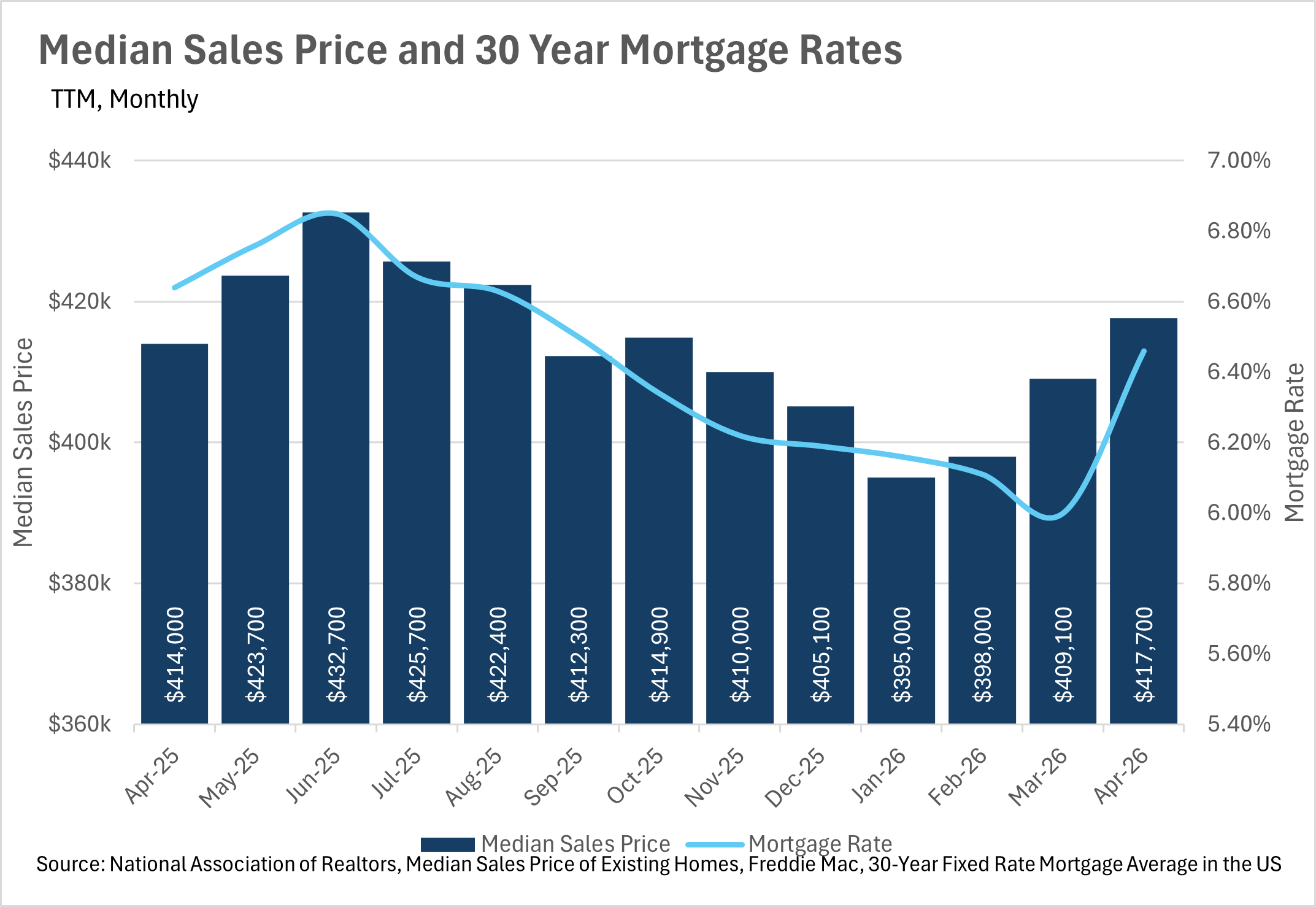

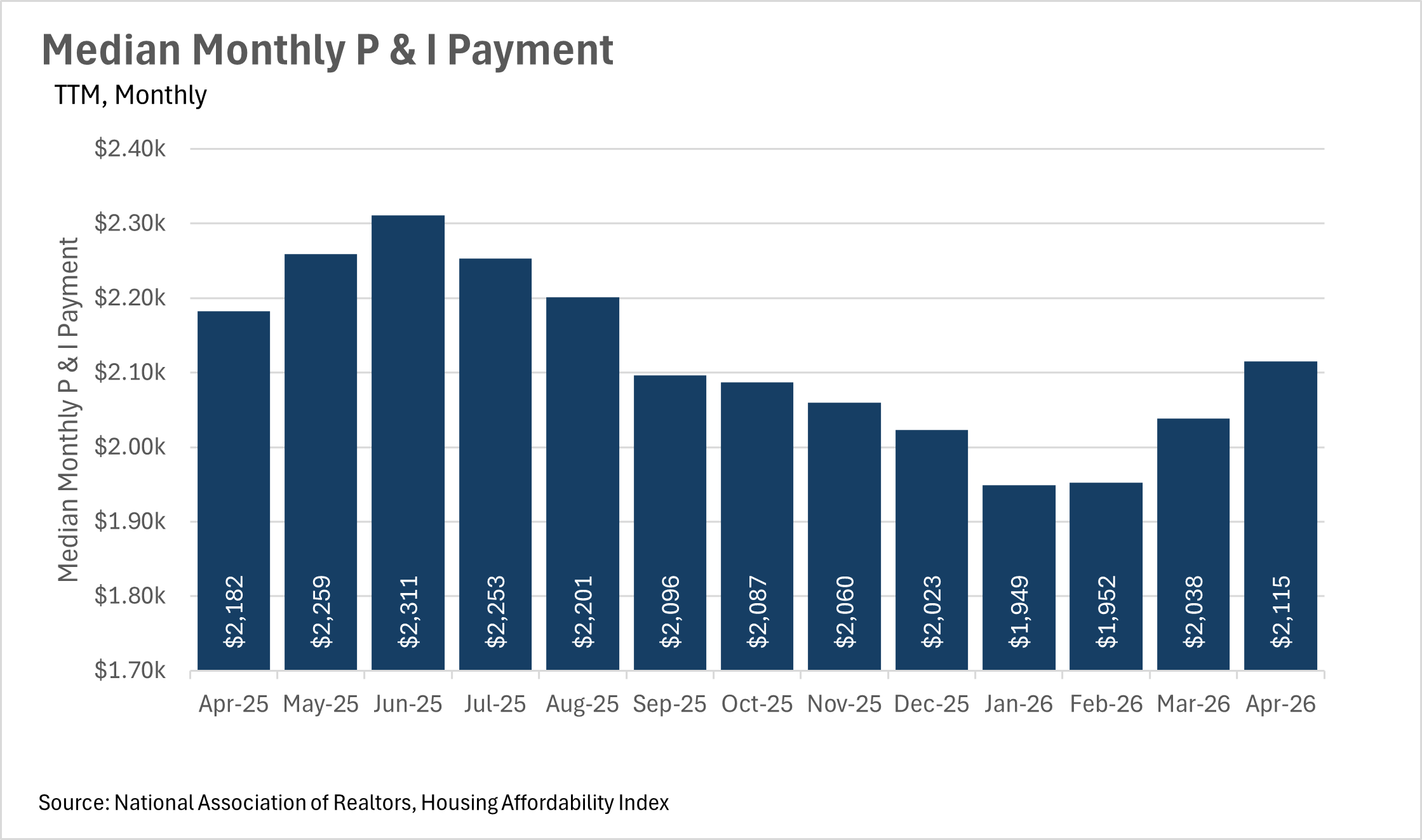

After several months of relatively flat price action, median home sale prices picked up some serious momentum in April. The median home sold for $417,700 in April, representing a 2.10% month-over-month increase and a 0.89% year-over-year gain. This bounce is especially notable when you consider that the median sale price had been on a downward trend from June of last year all the way through January, when it bottomed out at $395,000. Since then, we've seen three consecutive months of month-over-month increases, which tells us that the spring selling season is bringing some renewed energy to the market. However, it's worth noting that mortgage rates have ticked back up in recent weeks, with the average 30-year rate climbing to 6.46% in April, up from the 6.00% low we saw in March. This uptick in rates pushed the median monthly P&I payment up to $2,115, though this is still 3.07% lower than the $2,182 the median homeowner was paying at this time last year. If rates continue to climb, it could put a ceiling on how much further prices can rise in the near term.

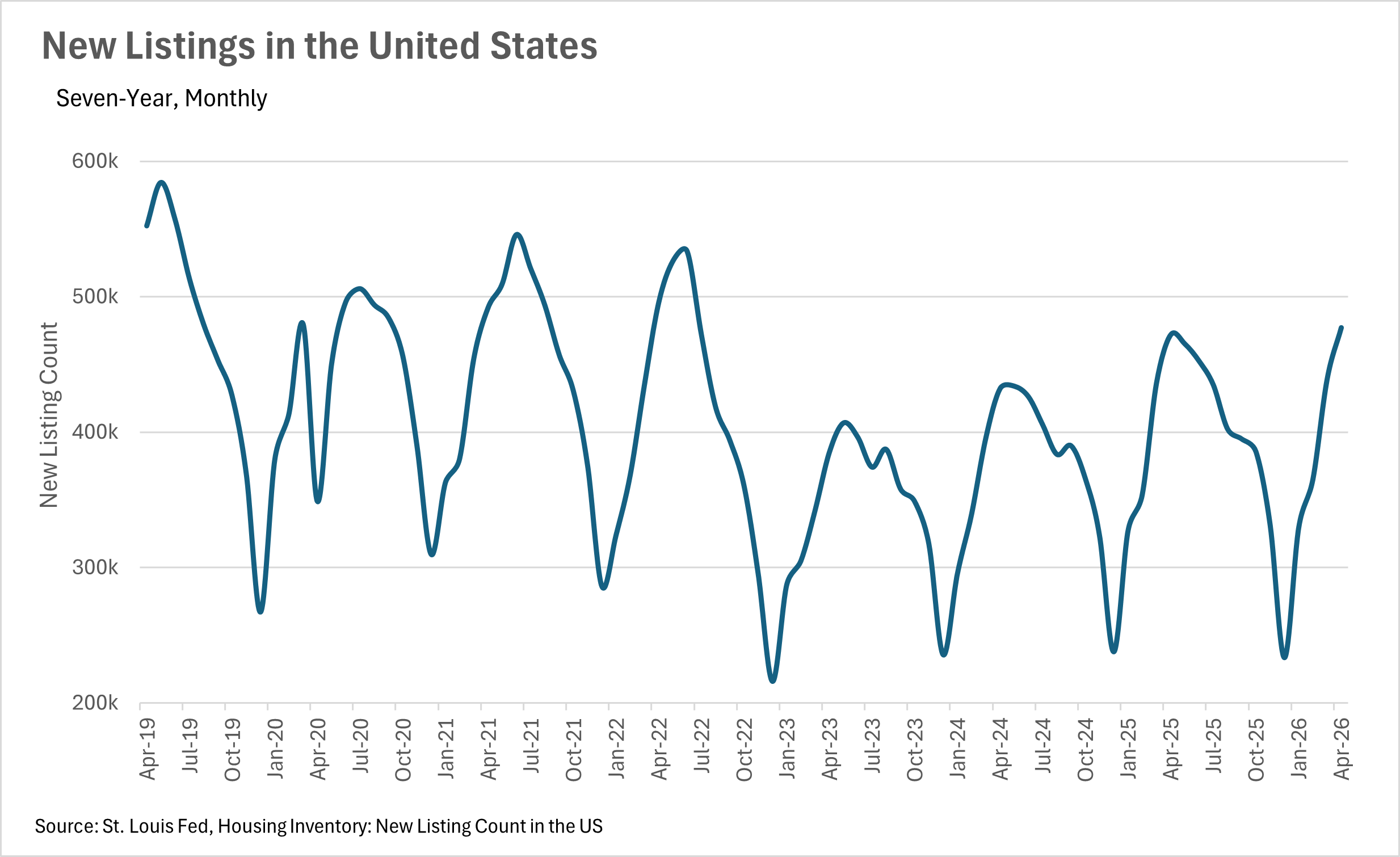

New listings are flooding the market as sellers get off the sidelines

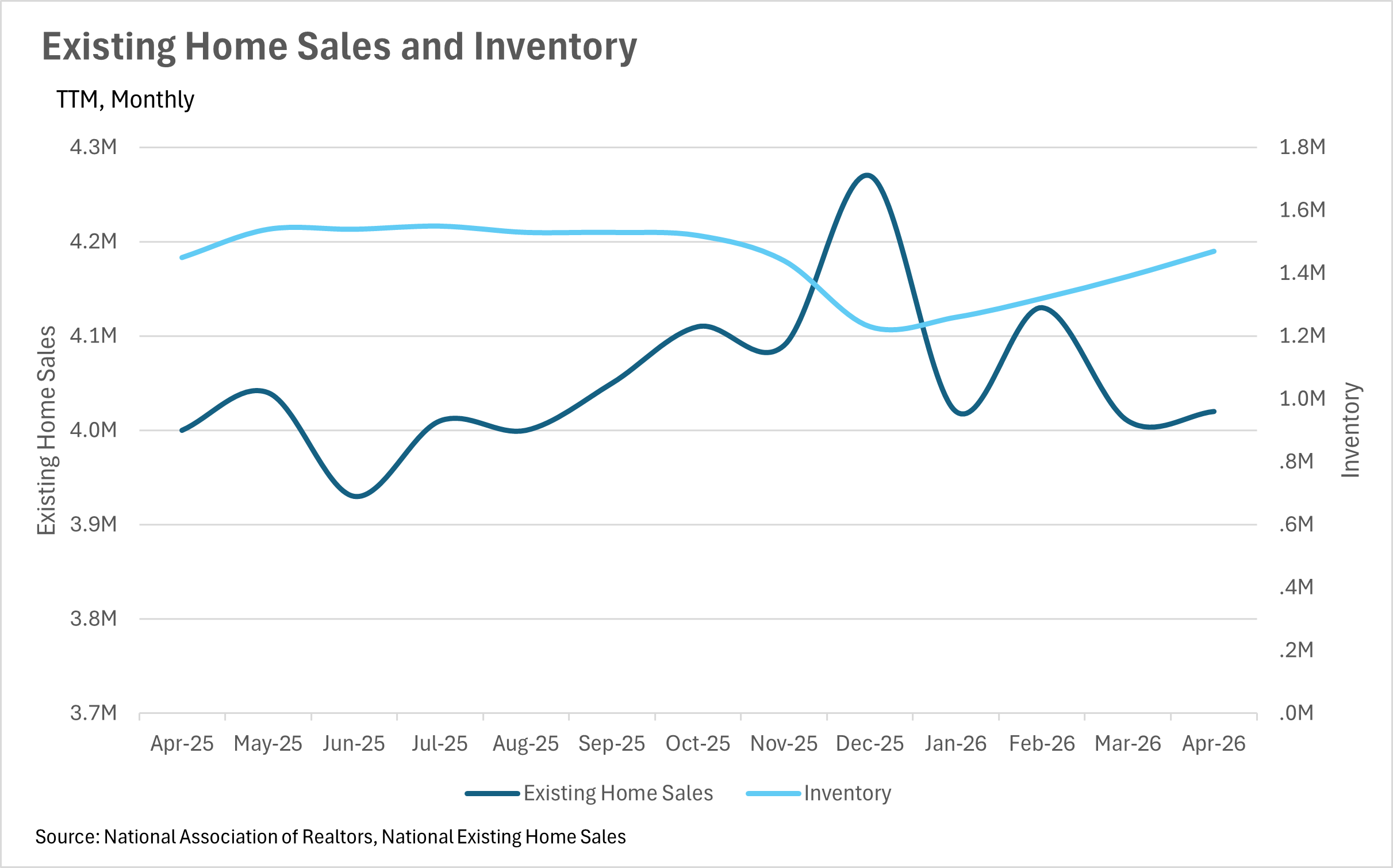

As the spring selling season heats up, we're seeing a significant wave of new listings hit the market. In April, there were 477,116 new listings nationwide, representing an 8.70% month-over-month increase and a 1.13% year-over-year increase. This influx of new listings is great news for buyers who have been dealing with limited options for the better part of the past few years. On the inventory side, there are now 1,470,000 homes available for sale, representing a 5.76% month-over-month increase and a 1.38% year-over-year increase. Inventory has been steadily building since its December low of 1,230,000, and we're now approaching the levels we were seeing during the peak of inventory season last summer. If this trend continues through May and June, buyers could find themselves with the most options they've had in quite some time, which would be a welcome shift in a market that has been starved for supply.

Existing home sales are holding steady, but buyers remain cautious

Despite the influx of new inventory and three consecutive months of rising prices, existing home sales have remained relatively flat. In April, 4,020,000 homes changed hands, representing just a 0.50% year-over-year increase and a 0.25% month-over-month uptick. While it's encouraging that sales are at least trending in the right direction, the pace of improvement has been glacial, which suggests that many buyers are still sitting on the sidelines. Part of the story here is the recent uptick in mortgage rates. After falling steadily from 6.85% last June to 6.00% in March, rates have bounced back to 6.46%, which may have given some prospective buyers cold feet. If rates stabilize or begin to decline again, we could see existing home sales pick up in a meaningful way as we move into the summer months. For now, though, it seems like buyers are content to wait and watch.

A balancing act heading into the summer

When determining whether a market is a buyers' market or a sellers' market, we look to the Months of Supply Inventory (MSI) metric. The state of California has historically averaged around three months of MSI, so any area with at or around three months of MSI is considered a balanced market. Any market that has lower than three months of MSI is considered a seller's market, whereas markets with more than three months of MSI are considered buyers' markets.

At the national level, we're seeing the market inch closer to a more balanced state. Inventory continues to build heading into the summer, while existing home sales have been essentially flat, meaning that the available supply is lasting a bit longer than it did at this time last year. However, the recent reversal in mortgage rates adds a layer of uncertainty to the equation. If rates continue to rise, we could see demand soften further, which would push the market toward buyers. On the other hand, if rates settle back down and buyers start to re-engage, the growing inventory could get absorbed quickly, keeping the market tilted in favor of sellers. As always, real estate is a highly localized asset, which is why you should check out what's going on in your local market below in the Local Lowdown!

Big Story Data

The Local Lowdown

Quick Take:

-

After two consecutive months of year-over-year declines, median sale prices bounced back into positive territory in March, climbing by 1.21%.

-

Inventory continues to build heading into the spring, with 3.85% more active listings on the market in April when compared to last year.

-

Listings are moving at a rapid pace, with the median listing spending just 21 days on the market, perfectly in line with where we were a year ago.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

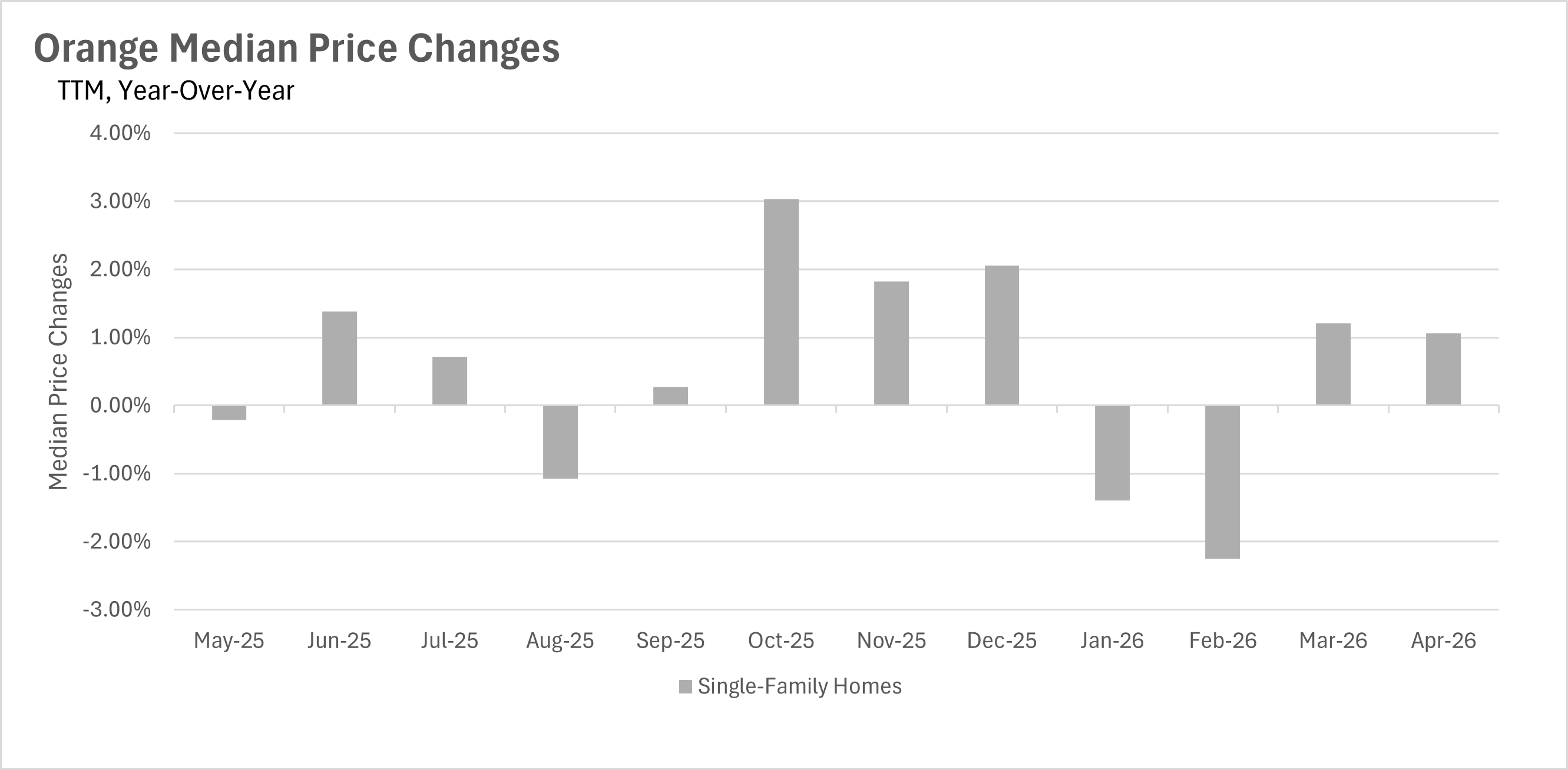

Orange County sale prices bounce back after a sluggish start to the year

After starting 2026 with back-to-back year-over-year declines in January and February, Orange County's median sale price roared back in March. The median single-family home sold for $1,467,500, representing a 1.21% year-over-year increase and the highest median sale price we've seen since June 2025. This bounce back is a welcome sign after the early-year softness, and it suggests that the pricing dip was more of a comp-related issue than a fundamental shift in the market. With the spring buying season now in full swing, it will be worth watching to see whether this upward momentum can sustain itself through the warmer months.

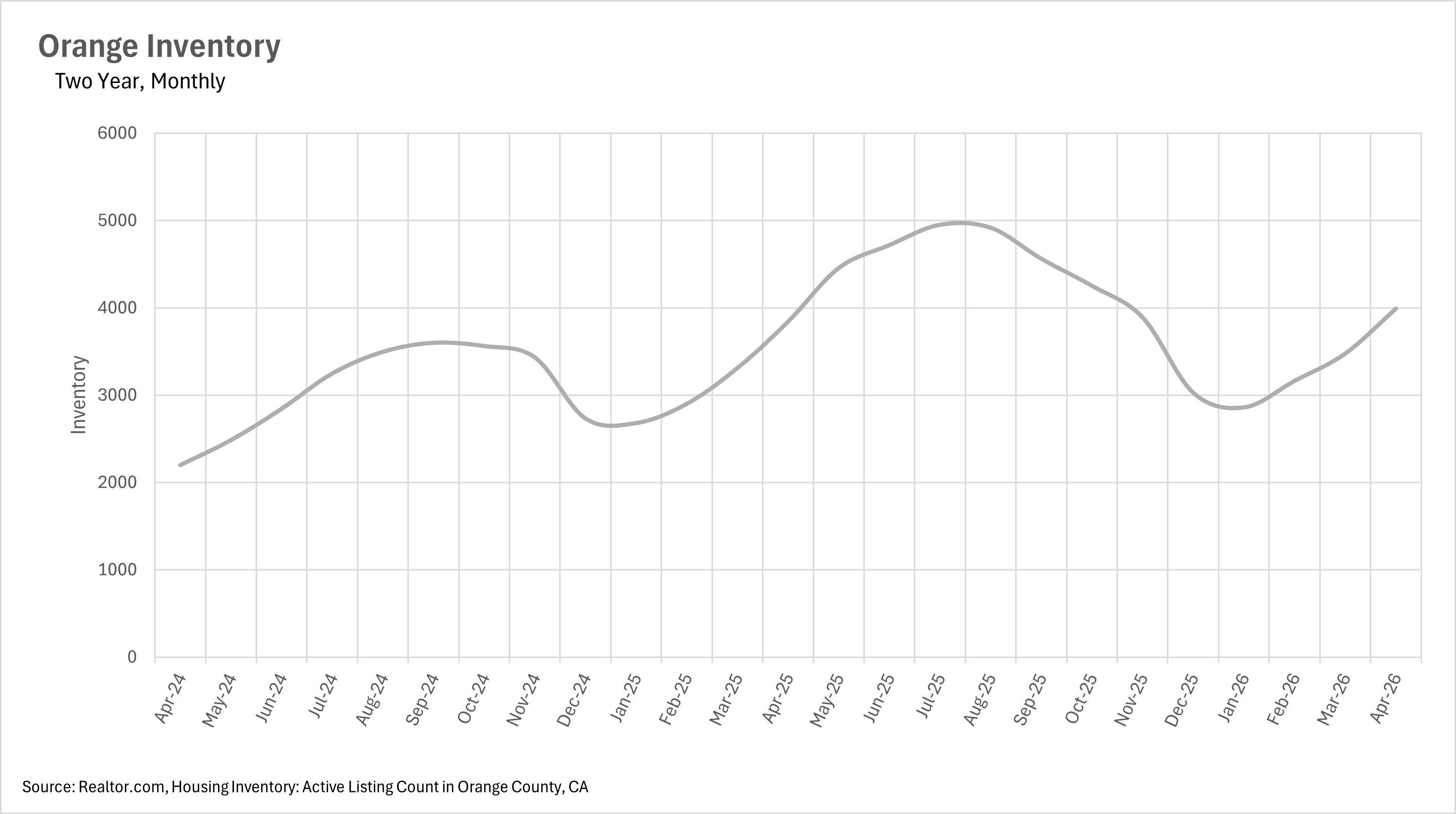

Inventory keeps building as sellers gear up for the spring rush

Inventory levels in Orange County continue to climb, as sellers look to capitalize on the spring selling season. In the month of April, there were 3,991 active single-family home listings on the market, representing a 3.85% increase on a year-over-year basis and a 14.78% increase on a month-over-month basis. This is now the third consecutive month of double-digit month-over-month inventory growth, which is right on track with the seasonal pattern we typically see as we move from winter into spring. That said, the year-over-year gap has narrowed quite a bit compared to earlier in the cycle, when we were regularly seeing inventory levels running 7% to 10% or more above the prior year. This suggests that the market is beginning to normalize, and the days of dramatically elevated inventory levels relative to the prior year may be coming to a close.

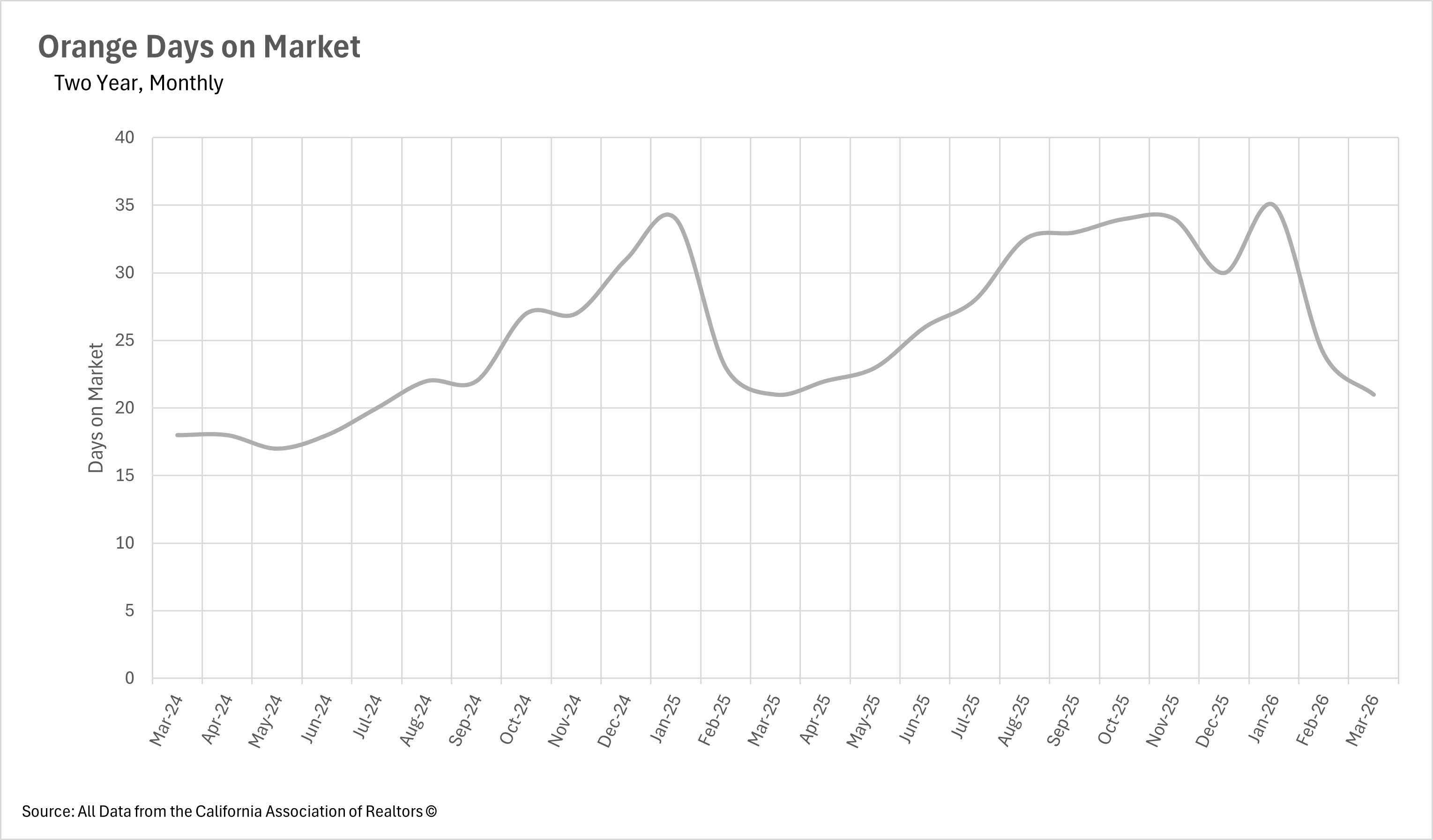

Listings are moving at last year's pace as demand ramps up

One of the more encouraging data points this month is the speed at which listings are moving off the market. In March, the median single-family home listing spent just 21 days on the market, which is perfectly flat on a year-over-year basis. This represents a 12.50% decline on a month-over-month basis, continuing the downward trend we've seen since January's cycle-high of 35 days. The fact that listings are moving this quickly despite elevated inventory levels is a clear indicator that buyer demand is strong heading into the spring season. Well-priced homes are not sitting around, and this pace of sales should give sellers confidence that the market is still very much active.

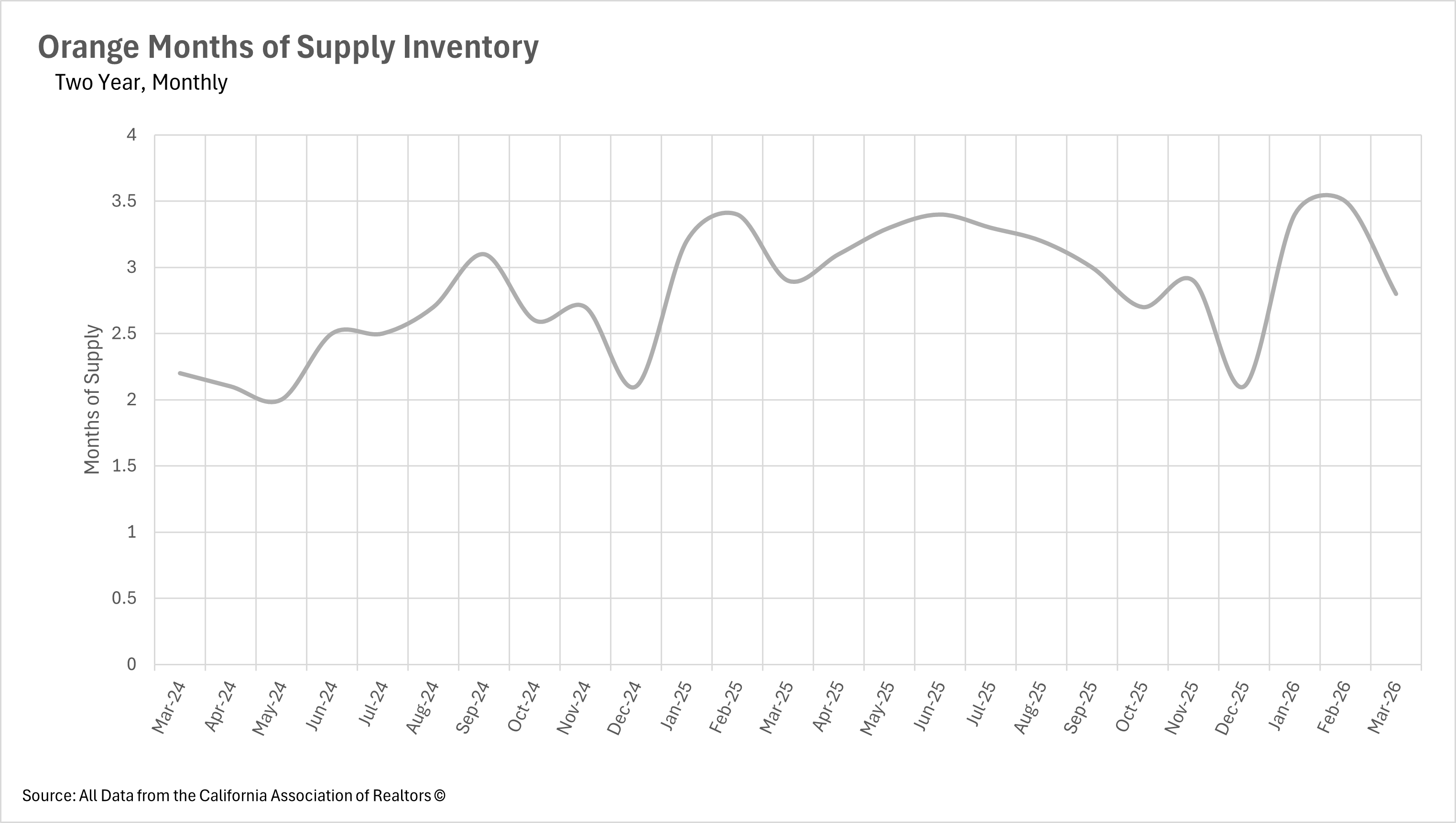

Orange County swings back to a seller's market

When determining whether a market is a buyers' market or a sellers' market, we look to the Months of Supply Inventory (MSI) metric. The state of California has historically averaged around three months of MSI, so any area with at or around three months of MSI is considered a balanced market. Any market that has lower than three months of MSI is considered a seller's market, whereas markets with more than three months of MSI are considered buyers' markets.

After spending the first two months of 2026 in buyers' market territory, Orange County has swung back to a seller's market as of March, with just 2.8 months of supply on the market. This represents a 20.00% decline on a month-over-month basis and a 3.45% decline on a year-over-year basis. This shift is a direct result of the strong buyer demand that we've been seeing as the spring season heats up. Even though inventory is continuing to build, demand is absorbing new listings at a rate that is pushing supply levels back below the three-month threshold. If this trend continues, we could see Orange County remain a seller's market throughout the busy spring and summer months.