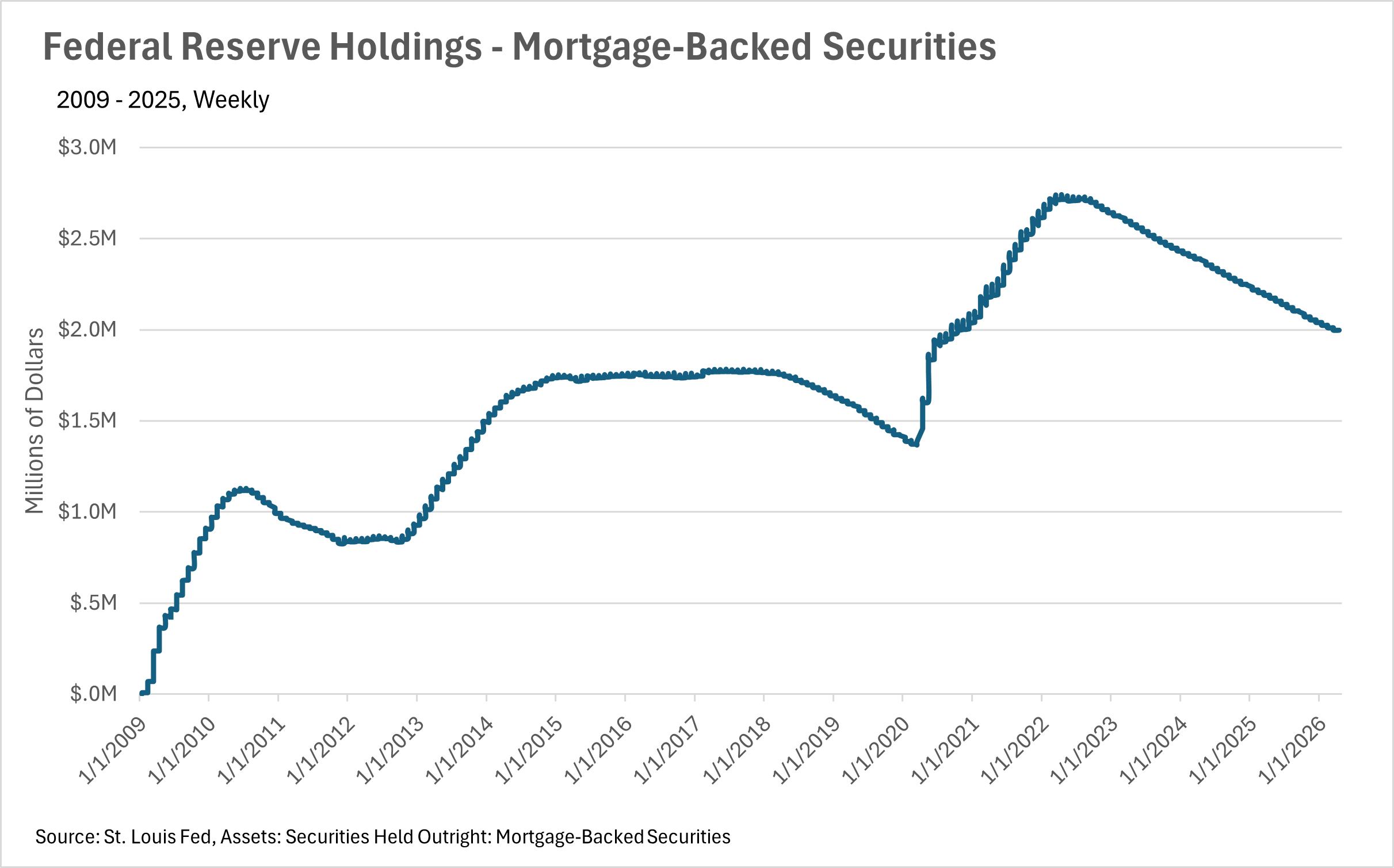

The Big Story

Quick Take:

-

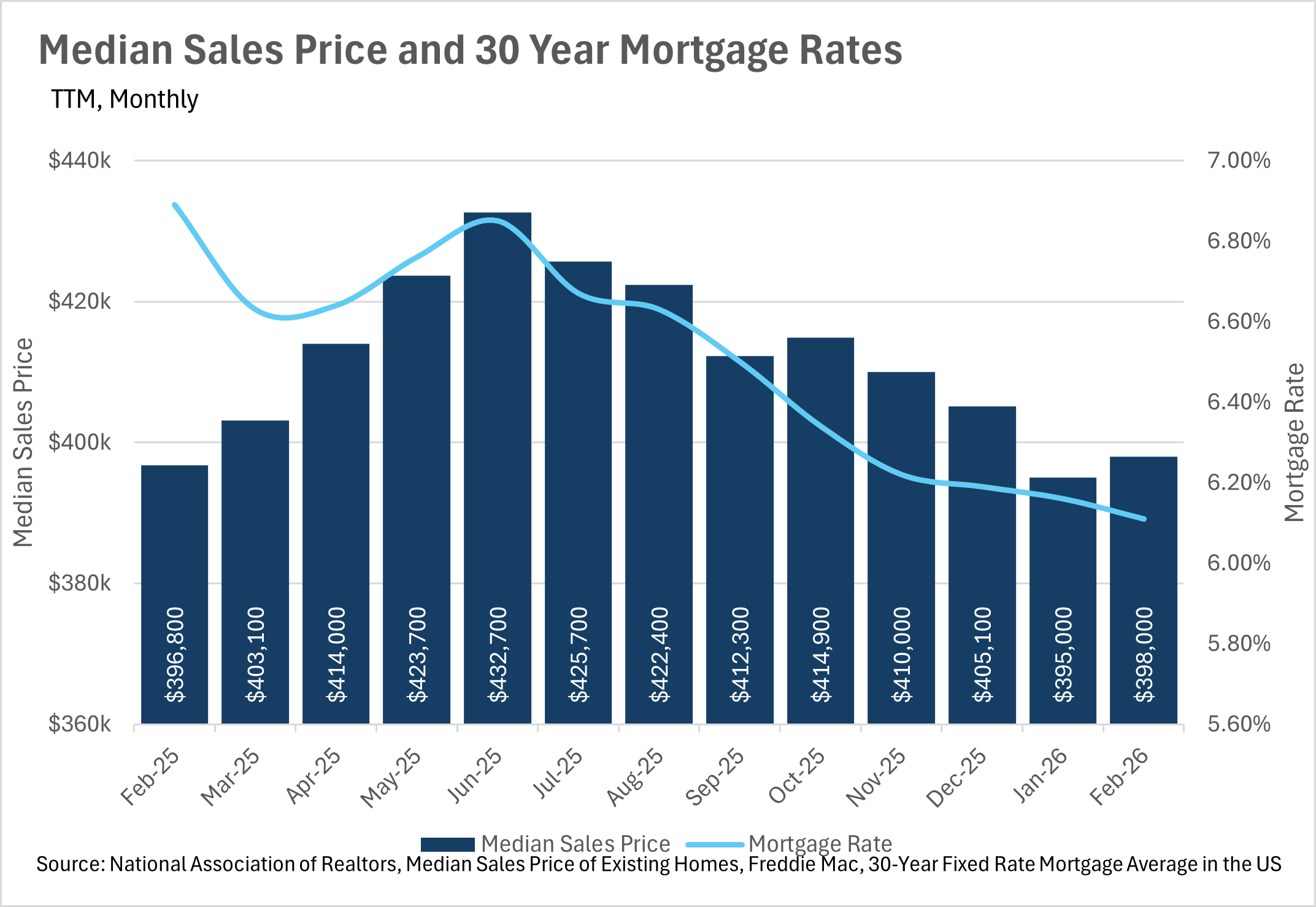

Median home sale prices ticked up slightly on both a month-over-month and year-over-year basis in February, continuing the holding pattern we've seen in recent months.

-

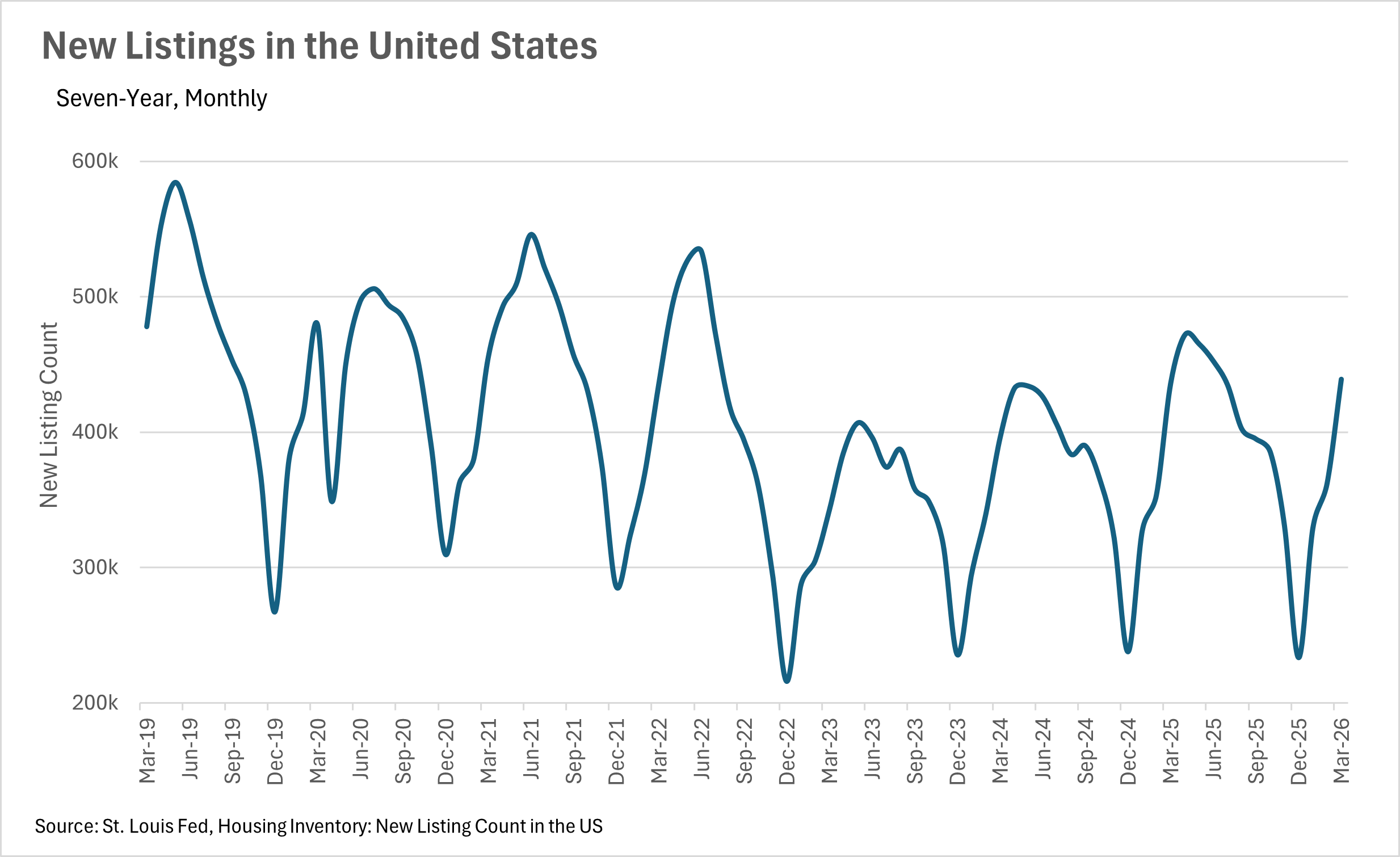

Inventory levels continue to climb modestly on a year-over-year basis, with new listings surging heading into the spring selling season.

-

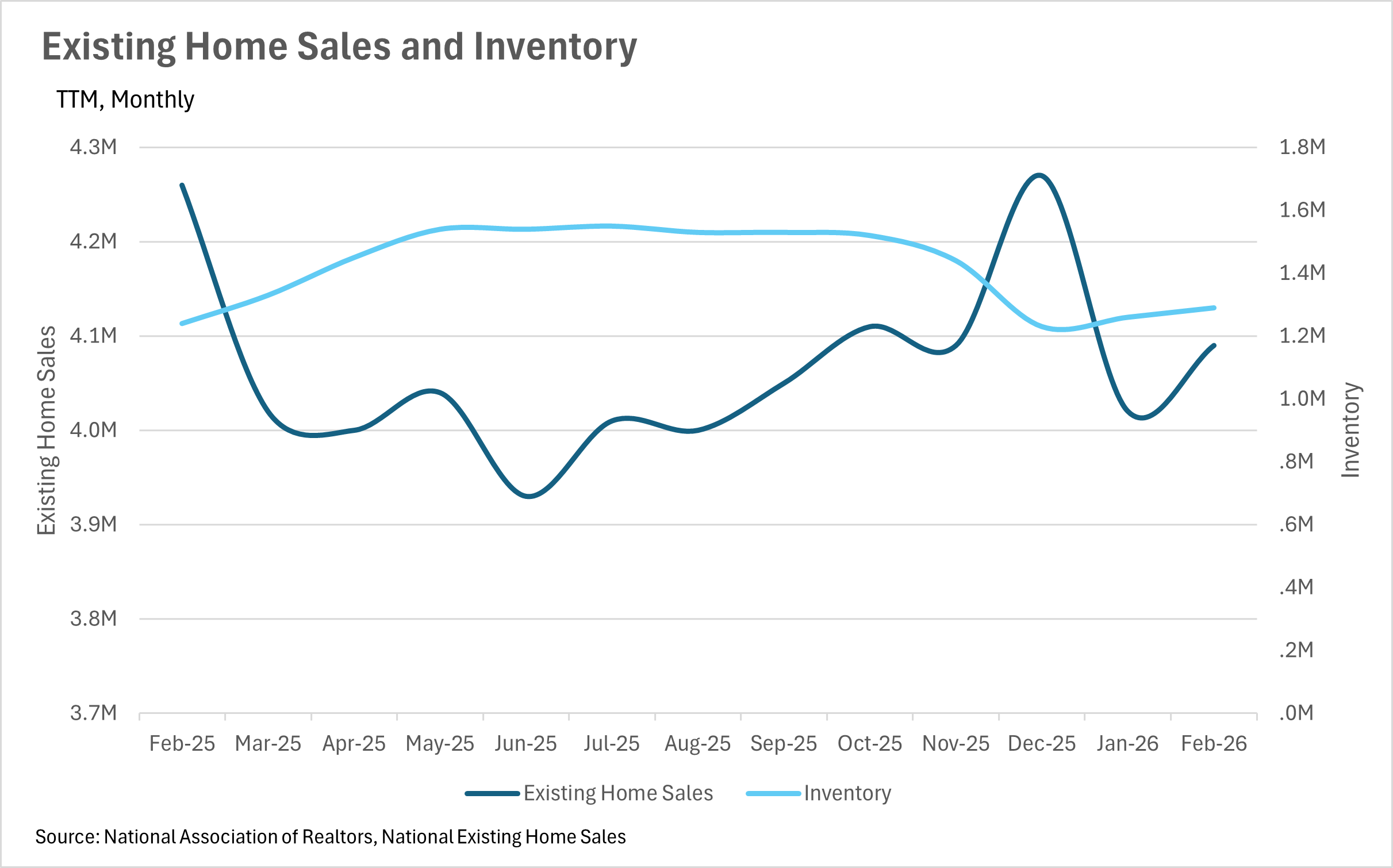

Existing home sales rebounded slightly from January, but remain below where they were at this time last year.

Note: You can find the charts & graphs for the Big Story at the end of the following section.

*National Association of REALTORS® data is released two months behind, so we estimate the most recent month's data when possible and appropriate.

Falling rates continue to ease the affordability crunch

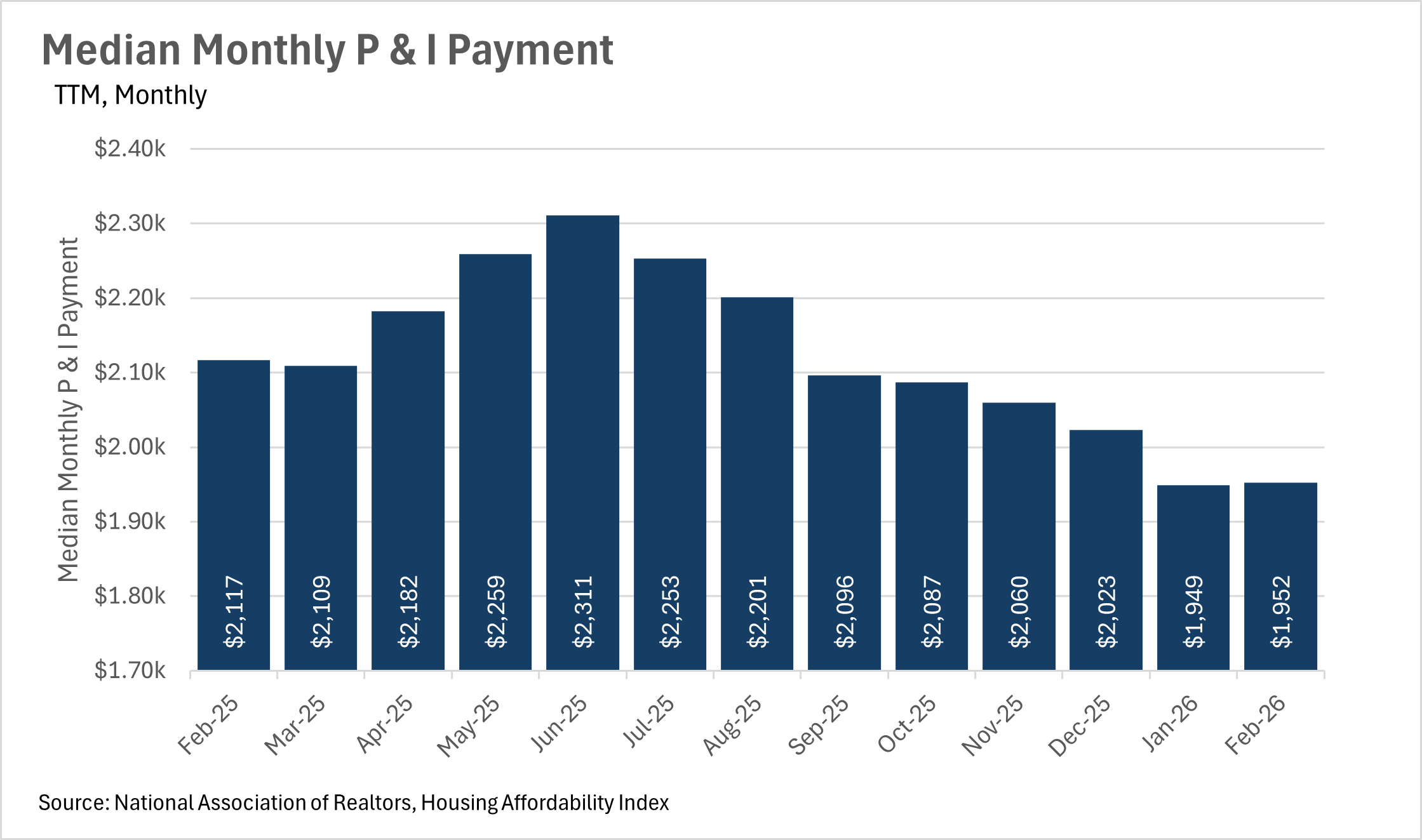

Although median home sale prices have remained remarkably stable over the past several months, the continued decline in mortgage rates is making homeownership considerably more affordable than it was just a year ago. In February, the median home sold for $398,000, representing a modest 0.30% year-over-year increase and a 0.76% uptick from January. On the mortgage rate front, the average 30-year rate dropped to 6.11% in February, representing an 11.32% year-over-year decline from the 6.89% we were seeing at this time last year. This decline in rates has had a major impact on what the average homeowner is paying each month. The median monthly P&I payment came in at $1,952 in February, down 7.79% from the $2,117 the median homeowner was paying just a year ago. That's approximately $165 in monthly savings, which is a significant boost to the average American's budget. If rates continue to trend downward, we could see buyers start to return to the market in a meaningful way as we move deeper into the spring and summer months.

New listings are surging as we head into the spring

One of the most encouraging stories in the housing market right now is the dramatic increase in new listings as we move into the spring selling season. In March, there were 439,000 new listings that hit the market, representing an eye-popping 21.21% month-over-month increase and a 0.70% year-over-year increase. This surge in new listings is a very welcome sight, as it means buyers will have considerably more options to choose from as the market heats up. On the inventory side, there were 1,290,000 homes available for sale in February, representing a 4.03% year-over-year increase and a 2.38% month-over-month increase. This gradual build in inventory, combined with the huge surge in new listings, should give buyers some breathing room as we head into the busier months of the year. That said, inventory levels still have a long way to go before they reach the levels we'd consider truly healthy, so it'll be worth keeping a close eye on whether this momentum carries through the spring.

Existing home sales are showing early signs of life

After a sluggish January, existing home sales rebounded slightly in February, with 4,090,000 homes changing hands. This represents a 1.74% month-over-month increase, but still comes in 3.99% below where we were this time last year. While it's certainly encouraging to see sales pick back up, the year-over-year decline tells us that buyers are still being cautious despite the substantial drop in mortgage rates that we've seen over the past year. Part of the story here may be that buyers are waiting to see even more rate cuts before they jump in, or they may be waiting for the influx of new listings to give them more options to choose from. Either way, it'll be fascinating to see whether the combination of lower rates, climbing inventory, and a fresh wave of new listings is enough to bring buyers off the sidelines in the coming months.

A market that's slowly tilting back toward balance

When determining whether a market is a buyers' market or a sellers' market, we look to the Months of Supply Inventory (MSI) metric. The state of California has historically averaged around three months of MSI, so any area with at or around three months of MSI is considered a balanced market. Any market that has lower than three months of MSI is considered a seller's market, whereas markets with more than three months of MSI are considered buyers' markets.

At the national level, we're seeing an interesting dynamic play out. Inventory is growing at a modest pace on a year-over-year basis, existing home sales are lagging slightly behind last year's figures, and new listings are surging into the market just as we head into the traditionally busy spring season. All of this suggests that the market is slowly tilting back toward a more balanced state, which would be welcome news for buyers who have been dealing with tight inventory for years. However, if mortgage rates continue to drop and buyers finally decide to come off the sidelines, we could just as easily see the market swing back in favor of sellers. As always, real estate is a highly localized asset, which is why you should check out what's going on in your local market below in the Local Lowdown!

Big Story Data

The Local Lowdown

Quick Take:

-

Median sale prices declined for the second consecutive month on a year-over-year basis, with the median single-family home selling for 2.25% less than it did last February.

-

Inventory continues its steady climb, with 7.00% more active listings on the market in March when compared to last year.

-

Listings are moving much more quickly than they were in January, with the median listing spending just 24 days on the market in February.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

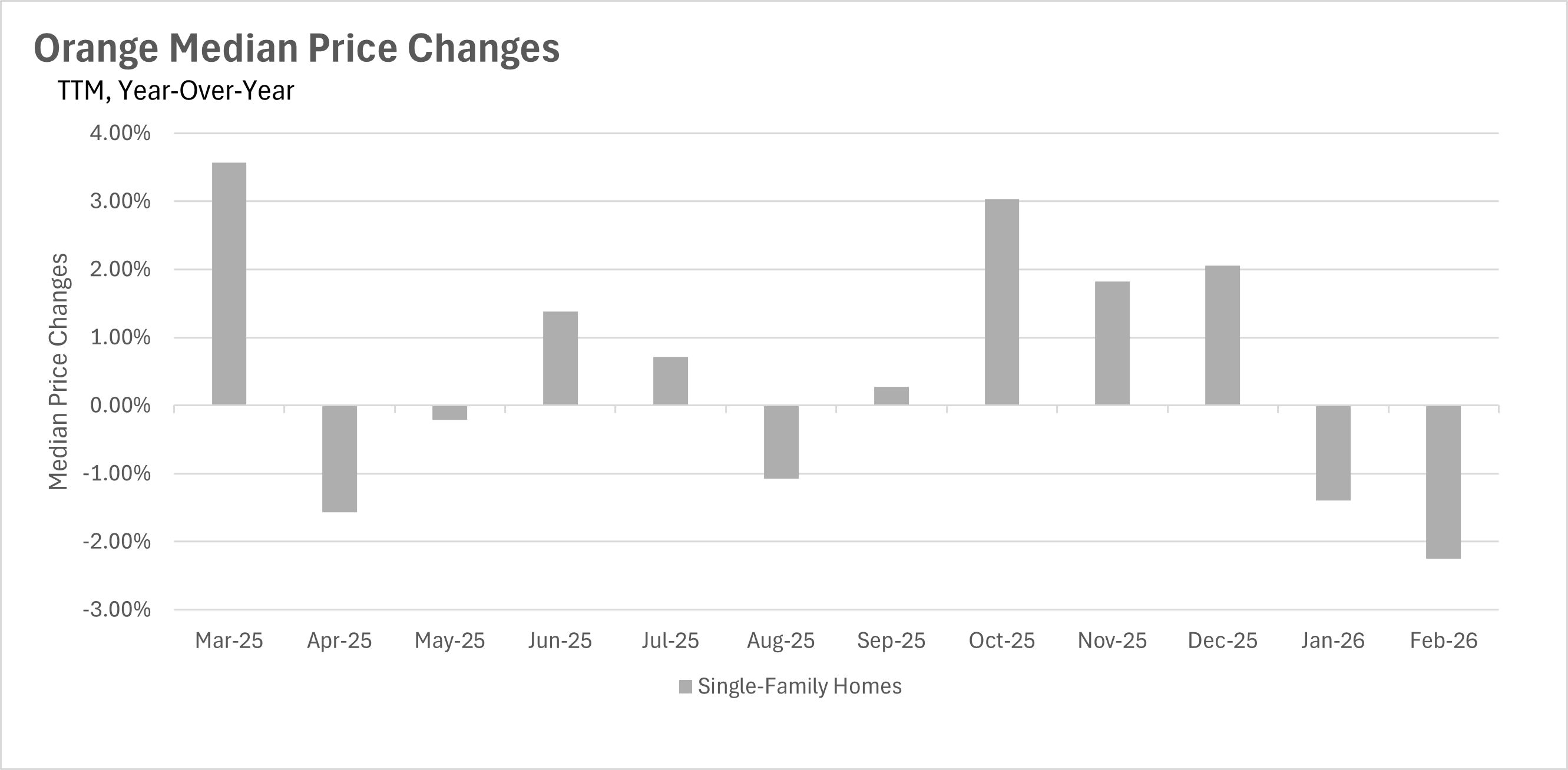

Orange County median sale prices continue to slide

After kicking off 2026 with a slight year-over-year decline in January, Orange County extended that trend into February, with median sale prices dropping by 2.25% on a year-over-year basis. The median single-family home sold for $1,432,500 in February, down from $1,465,500 during the same month last year. It's worth noting that the early months of 2025 were exceptionally strong for Orange County, with February 2025 representing the highest median sale price of the entire year, so the comparables Orange County is up against right now are genuinely tough to beat. With inventory continuing to build throughout the area, it wouldn't be surprising to see this softness in pricing persist for a bit longer before the spring and summer buying season heats up.

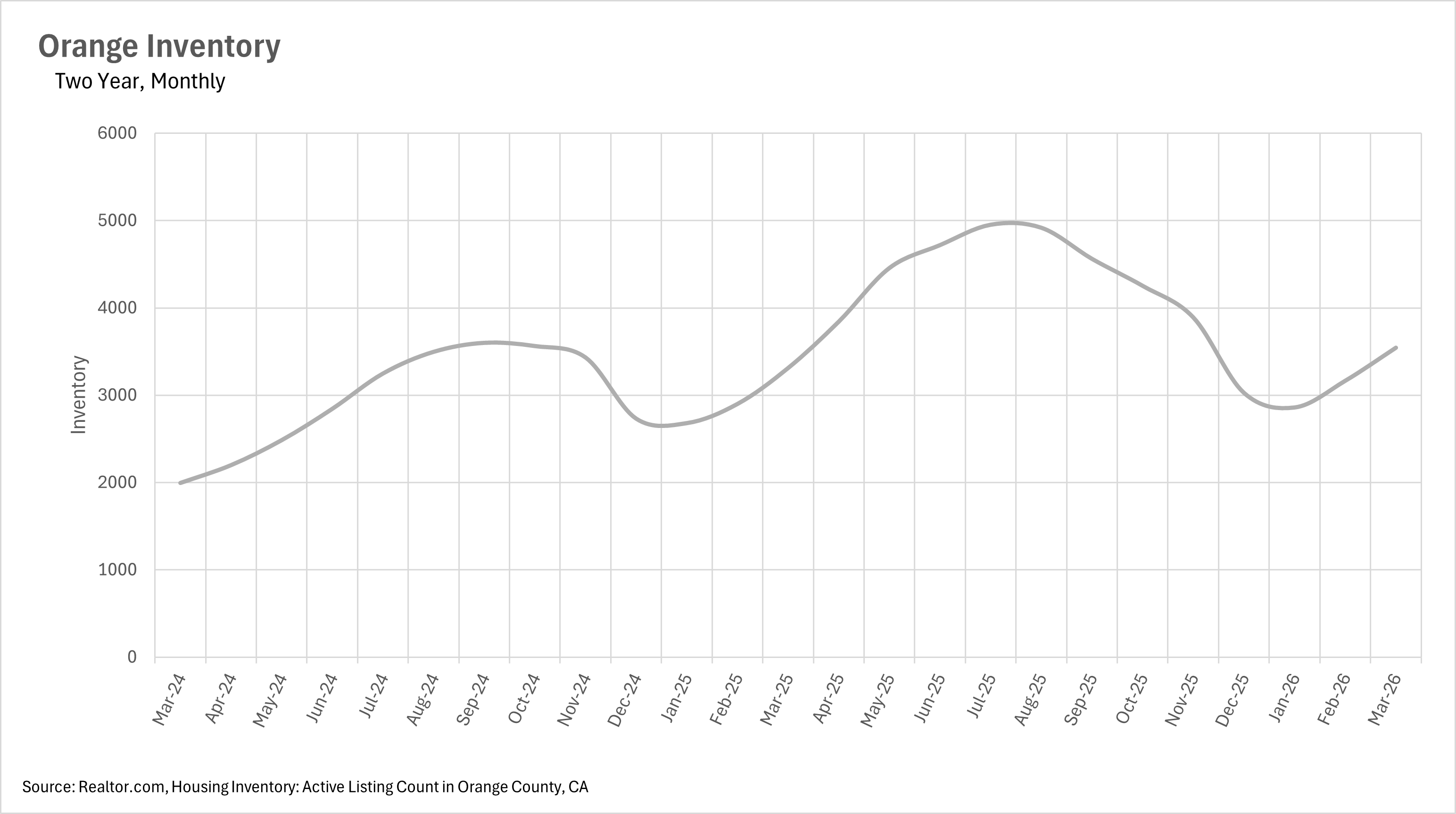

Inventory keeps climbing as we head deeper into spring

As we move past the seasonal lows of the winter, inventory in Orange County continues its steady climb back up. In the month of March, there were 3,544 active single-family home listings on the market, representing a 7.00% increase on a year-over-year basis and an 11.94% increase on a month-over-month basis. This is now the second consecutive month of double-digit month-over-month inventory growth, following February's 10.70% jump. While this pace of growth is typical for this time of year, as more sellers prepare to list heading into the busy spring season, the year-over-year increases signal that buyers will continue to enjoy a wider selection of listings than they had a year ago. That said, we're still well below the summer 2025 peaks, when inventory topped out at nearly 5,000 listings.

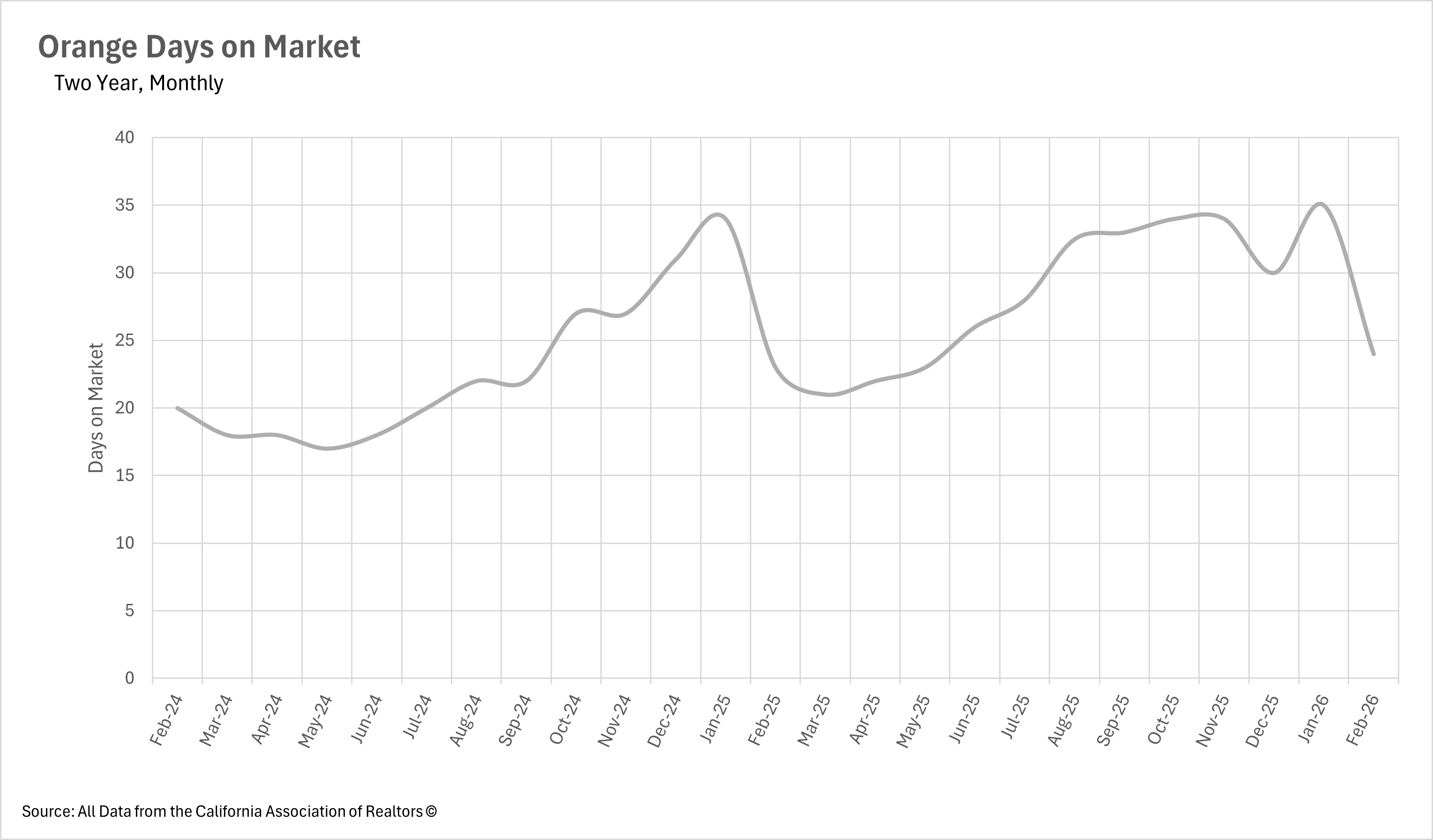

Listings are flying off the market once again

In a pretty dramatic turnaround from January, the median single-family home listing sat on the market for just 24 days in February. This represents a massive 31.43% decline on a month-over-month basis, and also shows that listings are now moving at speeds we haven't seen since much earlier in the cycle. On a year-over-year basis, days on market are up just 4.35%, which is a relatively modest increase all things considered. This is a clear sign that although inventory is building and prices have softened a bit, there is still plenty of demand on the buyer side, and the listings that are priced correctly are getting snapped up quickly. It will be interesting to see whether this pace holds as inventory continues to flood the market throughout the spring.

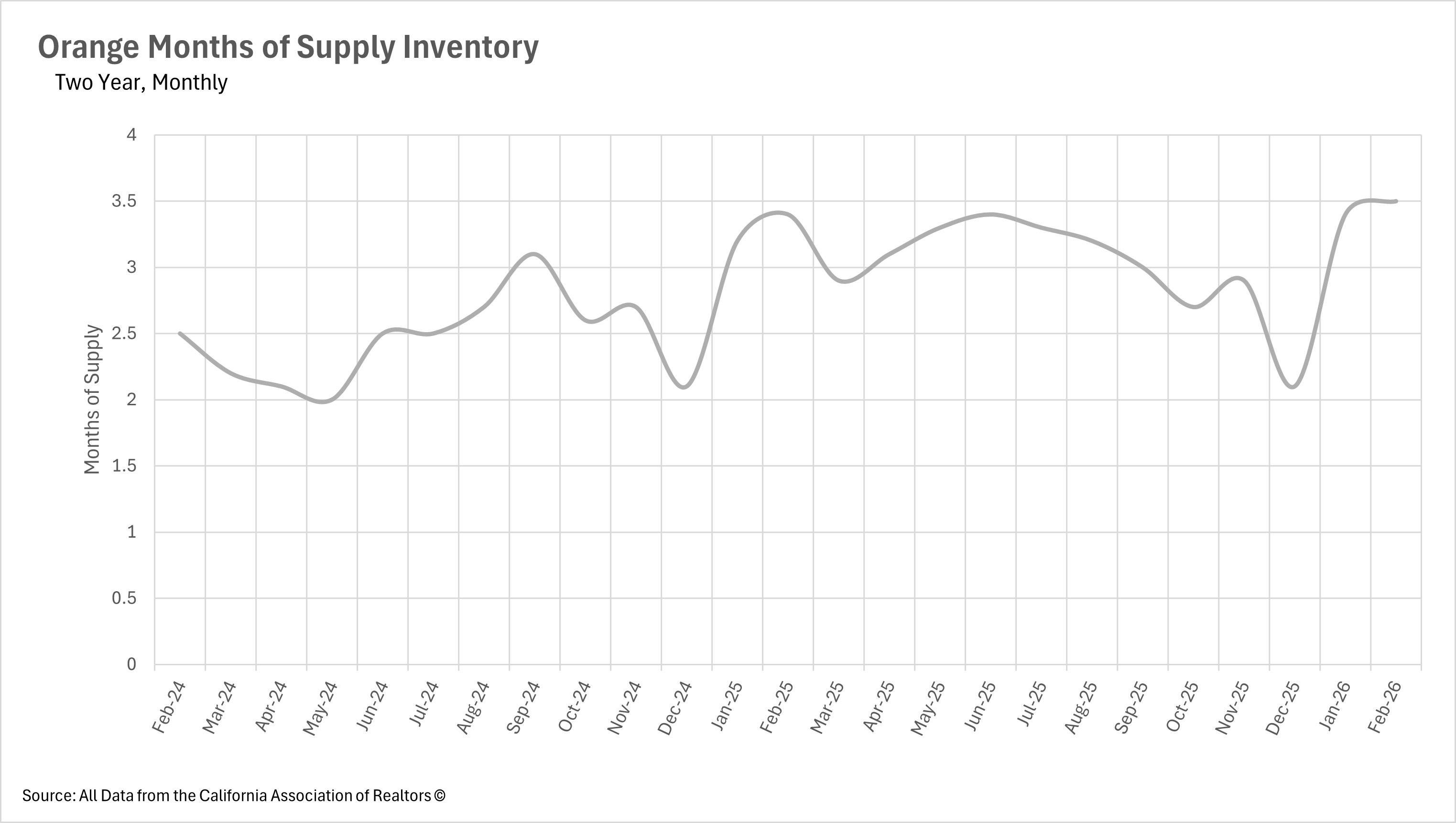

Orange County settles into balanced market territory

When determining whether a market is a buyers' market or a sellers' market, we look to the Months of Supply Inventory (MSI) metric. The state of California has historically averaged around three months of MSI, so any area with at or around three months of MSI is considered a balanced market. Any market that has lower than three months of MSI is considered a seller's market, whereas markets with more than three months of MSI are considered buyers' markets.

As of February, Orange County has 3.5 months of supply on the market, representing a 2.94% increase on both a month-over-month and year-over-year basis. This puts Orange County firmly in balanced market territory, leaning slightly toward being a buyers' market. After spending most of the back half of 2025 as a seller's market, the area has now seen two consecutive months of MSI above the three-month threshold to start 2026. With inventory continuing to build and the spring buying season just around the corner, it will be well worth watching whether Orange County remains balanced or if the influx of buyers is able to pull it back toward a seller's market.