The Big Story

-

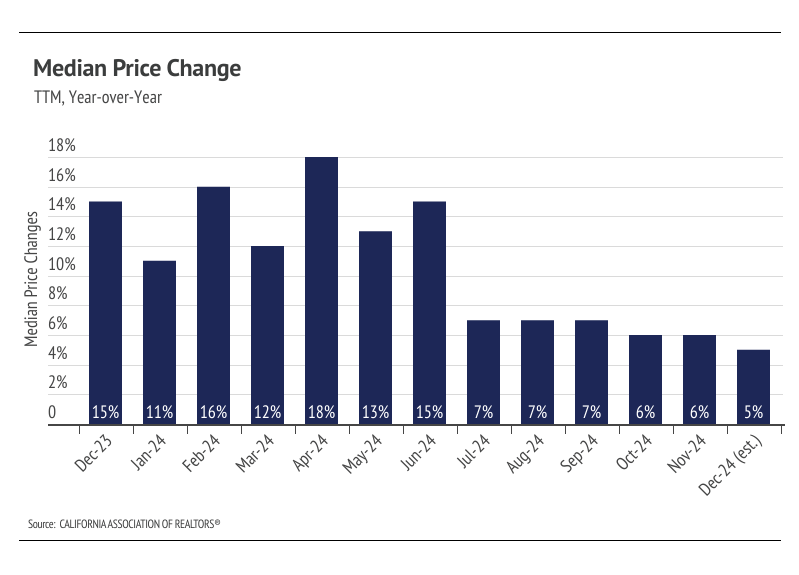

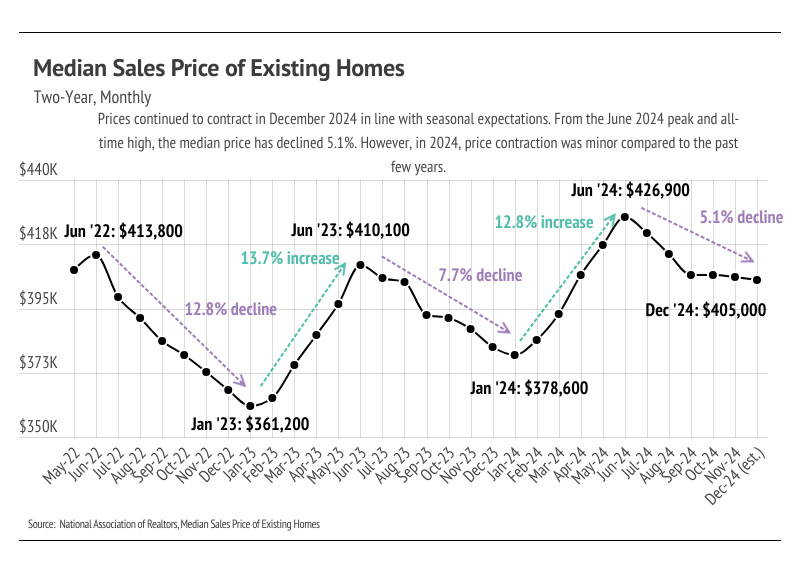

Home prices declined modestly in Q4 2024, showing atypical price stability in the second half of the year. Because prices didn’t contract significantly in the second half of 2024, they will easily rise to new highs in 2025.

-

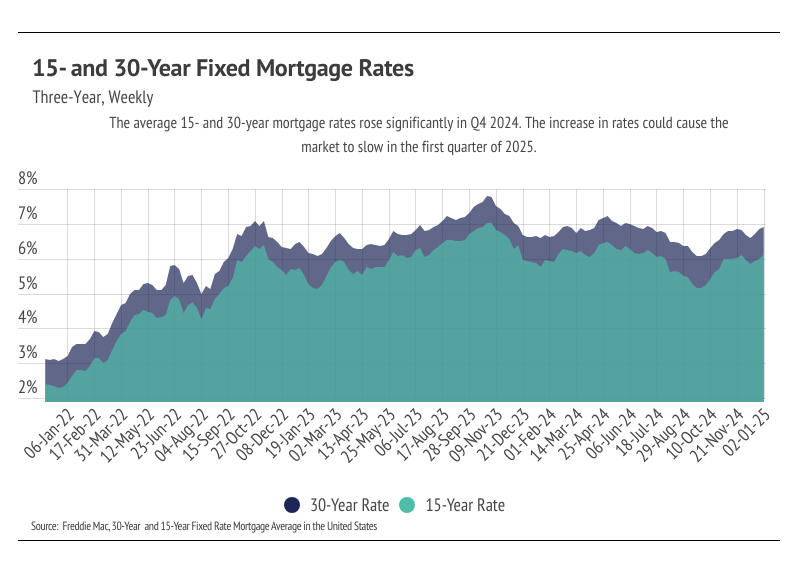

Since September 2024, the Fed has cut rates by 1%, bringing the interest rate that banks charge each other for short-term loans to a range of 4.25% to 4.5%. In 2025, we only expect the federal funds rate to decline by another 25 to 50 bps.

-

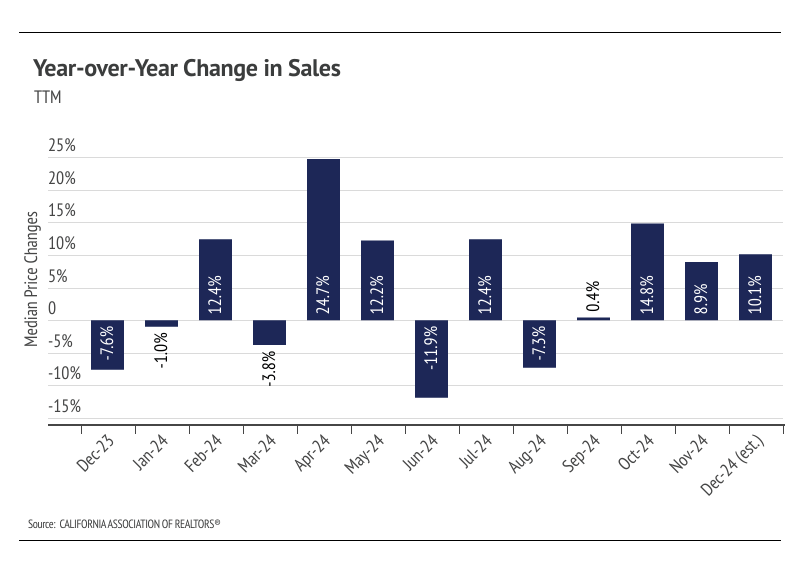

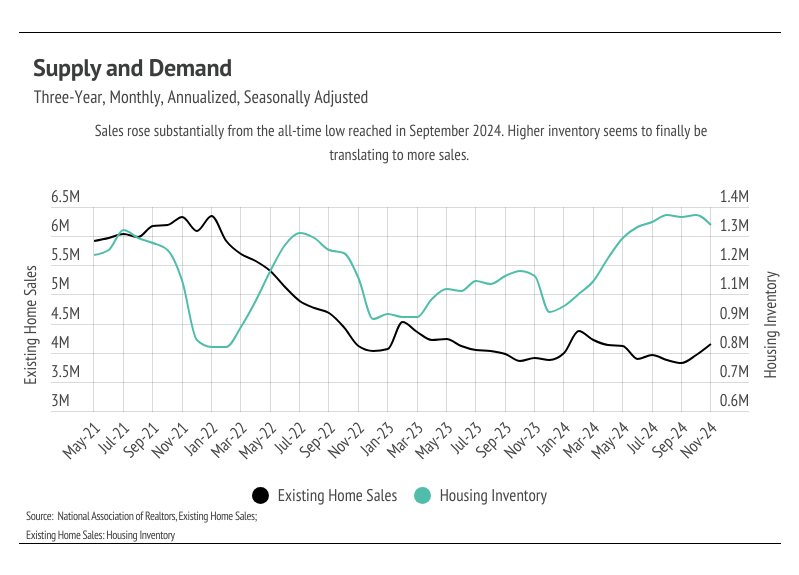

Sales rose 4.8% month over month, the swiftest pace since March. Sales accelerated 6.1% from one year ago, the largest year-over-year gain since June 2021. At the same time, inventory fell 2.9% but is still near its highest level in the past four years. Higher inventory levels created more opportunity for sales.

Big Story Data

The Local Lowdown

Quick Take:

-

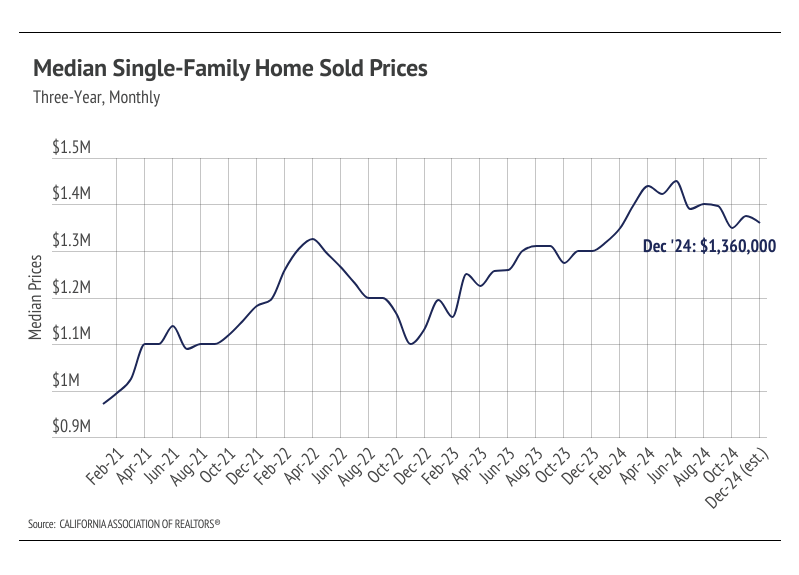

The median single-family home price declined in December, which is normal this time of year. We expect price contractions in January 2025 before climbing higher from February to June.

-

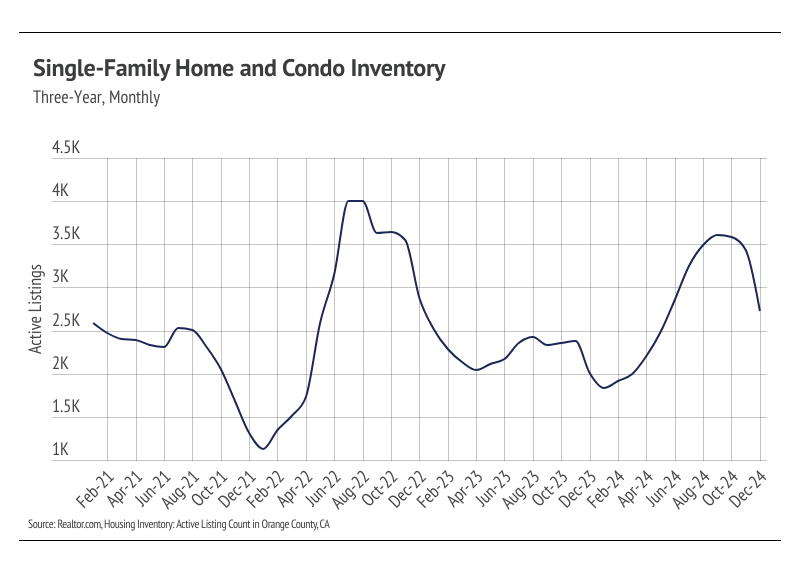

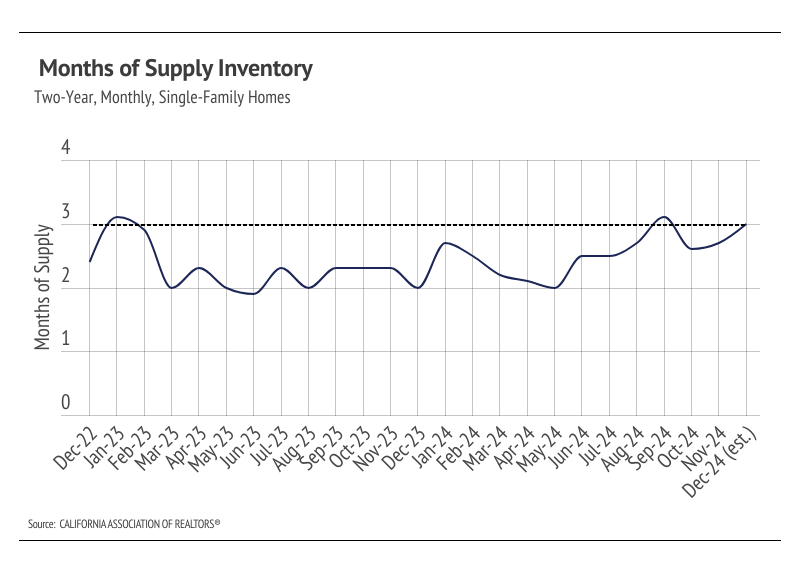

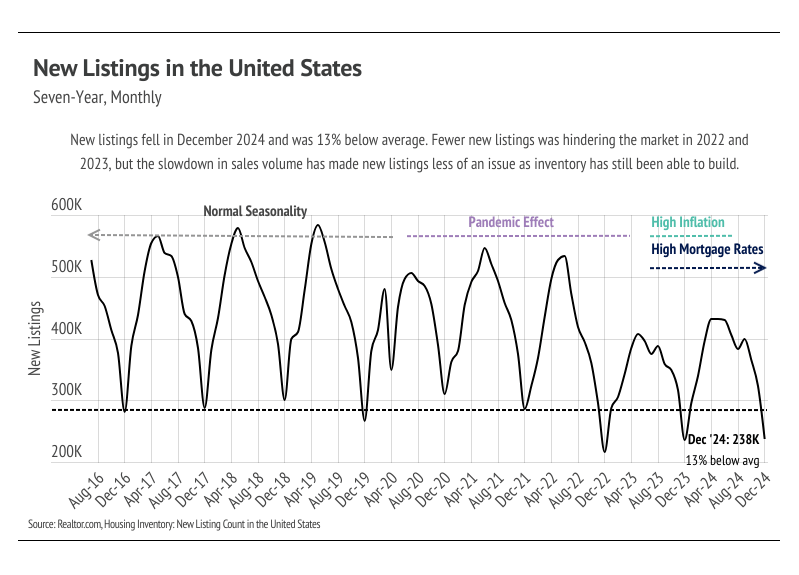

Inventory declined in December but has largely maintained the massive inventory gains from the first 10 months of the year. More homes on the market only benefits Orange County, which has been extremely undersupplied for the past four years.

-

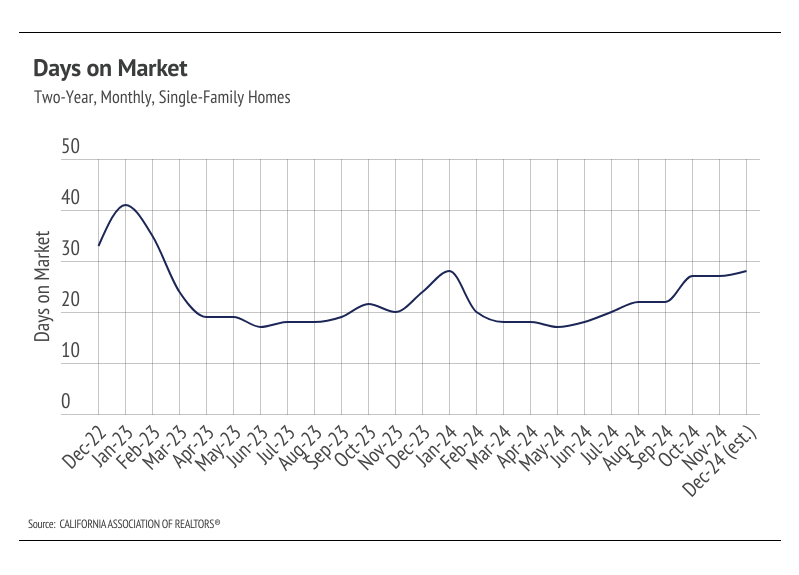

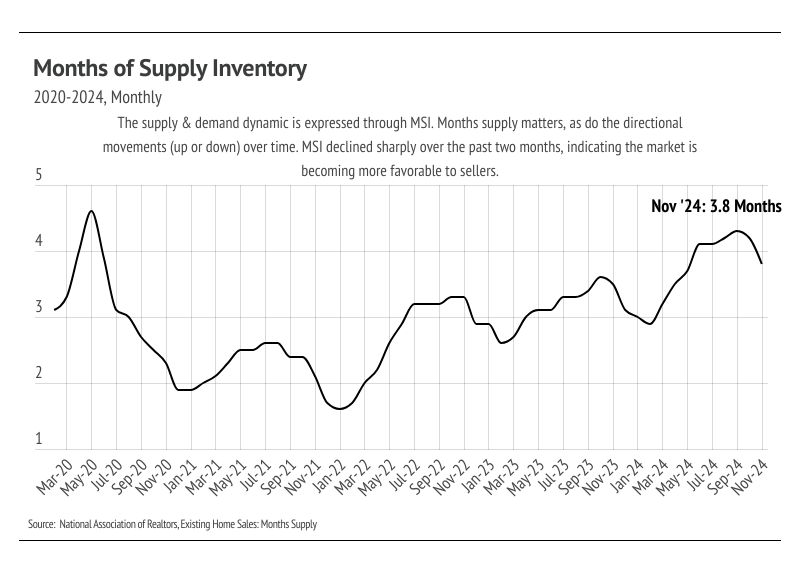

Months of Supply Inventory trended upward in 2024, closing out the year at three months of supply. MSI now indicates the market is more balanced between buyers and sellers.

Local Lowdown Data